IATA April 2026 Passenger Market Analysis: First Post-Pandemic Demand Contraction at -3.4% — Five Charter Implications for Korean HNW Principals

Published: May 29, 2026 | Read time: 16 minutes | Format: IATA monthly market analysis and Korean charter decision framework

📊 Executive summary

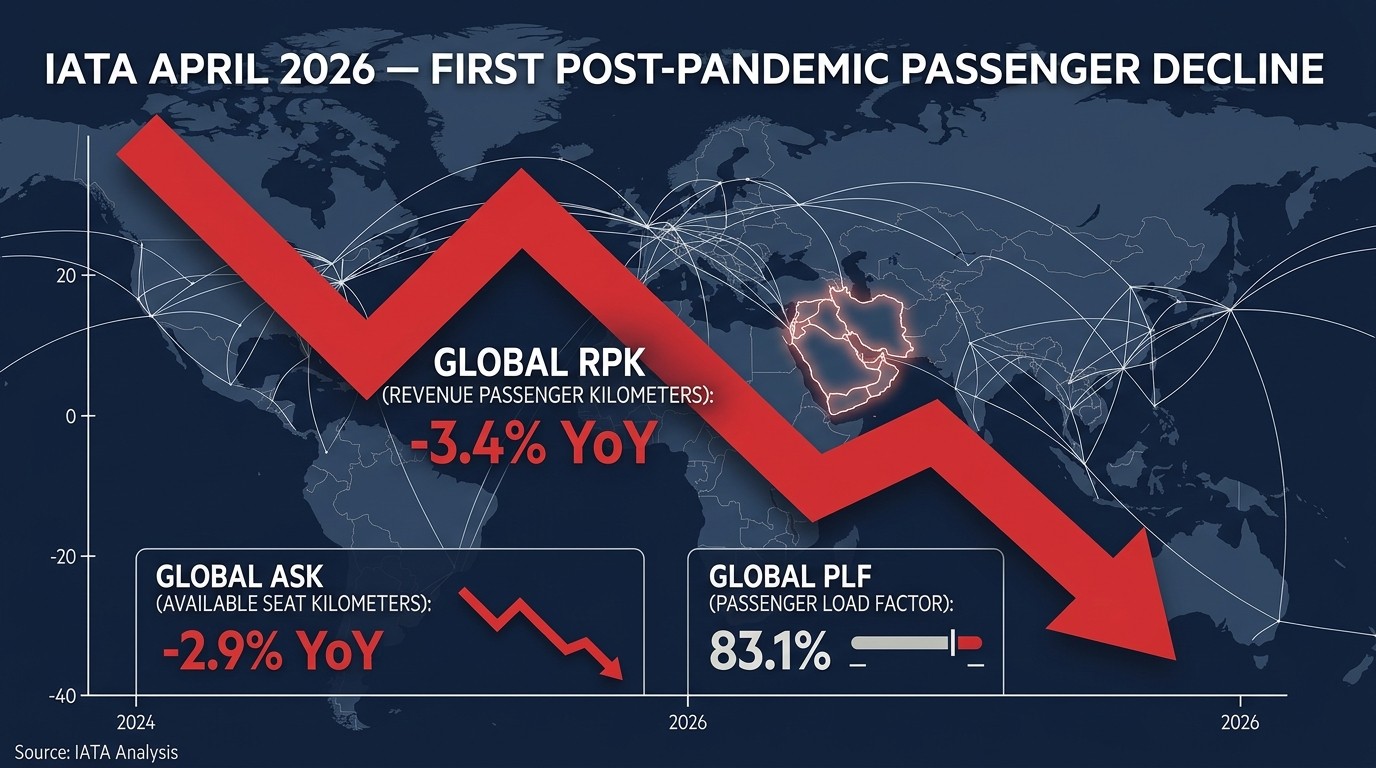

✔️ IATA's April 2026 data marks the first post-pandemic global passenger contraction: RPK -3.4% YoY

✔️ Middle East -46.6% (vs March's -59.2%, modest easing), international -5.3%, domestic essentially flat

✔️ May forward schedules show further -1.1% capacity decline; June recovery forecast at a thin +0.2%

✔️ Commercial seat availability and route flexibility are tightening; principals reorganizing May-June travel is rational

✔️ ACK distills the April reading into five concrete charter implications for Korean HNW principals and executives

→ May-June charter advisory (Wonjin Choi 📞 +82-10-7723-3177)

IATA April 2026 Passenger Market Analysis: First Post-Pandemic Demand Contraction at -3.4% — Five Charter Implications for Korean HNW Principals

The International Air Transport Association's April 2026 release tells a single, important story: the post-pandemic recovery has paused. Industry RPK fell -3.4% year-on-year, capacity (ASK) was down -2.9%, and the load factor slipped to 83.1% — the first PLF decline of 2026. After eighteen months of recovery momentum through late 2024 and all of 2025, April is the first month where the global passenger market actually contracted. The drivers were specific: Iran-related Middle East airspace disruption, jet fuel costs more than doubling year-on-year, and Easter shifting into early April, draining the late-month transatlantic peak.

IATA Director General Willie Walsh summarized the read this way: "The 46.6% fall in demand for carriers in the Middle East due to war in the region was so acute that it dragged overall demand down -3.4%. The situation for air transport remains highly volatile. The cost of jet fuel more than doubled in April, which is pushing airfares up. Forward schedule data is showing a reduced offering in the coming months, indicating that airlines are balancing high fuel costs and weaker demand." Translated to operational reality for principals flying out of Korea: commercial seat supply, route stability, and fare predictability are all at their tightest point of the first half of 2026.

For Korean HNW principals and corporate executives, the implications are direct. Incheon-Europe commercial flights are rerouting around closed Middle East airspace, adding 1-3 hours of block time. May seat capacity will contract further than April. The June recovery is thin enough that summer pricing through July and August won't settle in time. Any May-June itinerary still reliant on commercial first or business class is exposed simultaneously to schedule change risk, seat availability risk, and pricing risk. This page translates IATA's April release into five concrete charter implications for Korean principals, plus a route-by-route commercial-vs-charter decision matrix for the May-June window.

What's covered: IATA's headline metrics (RPK, ASK, PLF), the international-vs-domestic split, six-region performance with Middle East and Latin America at opposite ends, the most-affected routes, May-June forward schedules, the five charter implications for Korean principals, and a commercial-vs-charter decision matrix across six typical Korean executive travel scenarios. This piece extends the March 2026 IATA analysis already published, focusing on what changed in April and what principals should do about it now.

Air Charter Korea (ACK) runs a single consulting channel translating IATA monthly market data into actual flight decisions for Korean HNW principals and corporate executives. Founder Wonjin Choi serves as the Victor × Air Charter Service Korea Agent, connecting global market intelligence to Korean principal flight patterns each month, so that route, operator, and timing decisions get made ahead of market volatility rather than after.

⚡ May-June charter advisory: free intake

If you have May or June travel to the Americas, Europe, or the Middle East, ACK runs a free pre-review applying IATA's April data to your itinerary, with operator matching and routing strategy. With commercial capacity tightening, locking in May's critical flights is the simplest way to preserve schedule control.

📧 contact@aircharterkorea.com | 📞 Wonjin Choi +82-10-7723-3177

→ Free May-June charter advisory

1. Three Headline Indicators: What April's First Contraction Means

Industry-wide metrics

Indicator | April 2026 | What It Means |

|---|---|---|

RPK (Revenue Passenger Kilometers) | -3.4% YoY | First contraction of the post-pandemic recovery; 748 billion RPK total |

ASK (Available Seat Kilometers) | -2.9% YoY | Capacity contracting too, but not as fast as demand |

PLF (Passenger Load Factor) | 83.1% | Down -0.4 ppt YoY; first PLF decline of 2026 |

Seasonally adjusted RPK | -2.7% YoY | Contraction holds after removing seasonal effects |

Sequential MoM | -0.1% | Further softening from March, trend weakening |

Why falling RPK signals real demand weakness

RPK multiplies passengers carried by the distance they flew. A decline can come from fewer travelers, shorter trips, or both. April's -3.4% is meaningful because ASK only contracted -2.9%, meaning seats are pulling back but slower than demand — which produces empty seats and pressure on yields. Airlines respond to that pressure in one of two ways: discount fares to fill seats, or consolidate routes and pull aircraft. Both responses make commercial scheduling less reliable for executive travelers.

The significance of 2026's first PLF decline

PLF — the share of available seats actually sold — held flat or rising through Q1 2026. April's drop to 83.1% is the year's first directional change. The level remains high in absolute terms, but the trajectory is what matters. As load factors soften, carriers face the choice between cutting prices or cutting capacity. Either path produces less stability in the timing and inventory an executive sees when trying to book a specific Seoul-to-LA or Seoul-to-London routing.

2. International vs Domestic: -5.3% International Contraction, Domestic Essentially Flat

Segment | Market Share | RPK YoY | ASK YoY | PLF |

|---|---|---|---|---|

International | 62.8% | -5.3% | -5.1% | 83.9% |

Domestic | 37.2% | -0.04% | +0.8% | 81.9% |

International -5.3%: Sharp deterioration from March

International RPK fell from March's -0.6% to April's -5.3%, a significant deterioration. International accounts for 62.8% of the global market, so this segment is doing most of the work to pull the headline contraction down. For Korean principals, this is the segment that matters most: every Incheon long-haul and most Gimpo international routes sit in this bucket, where premium cabin availability and ticket pricing are both under pressure as carriers reshape schedules.

Domestic essentially flat, but with wide market dispersion

Domestic was flat overall, cooling sharply from March's +6.6%. The market-level dispersion is wide: Japan +3.7% leads, India -2.9% trails. China cooled from +13.7% in March to +1.2% in April as the Lunar New Year boost faded, and Australia flipped from +8.8% in March to -0.4% in April. Higher domestic volatility means that even Korean short-haul Japan and China travel — usually reliable on commercial — faces some pricing and availability fluctuation if it depends entirely on scheduled service.

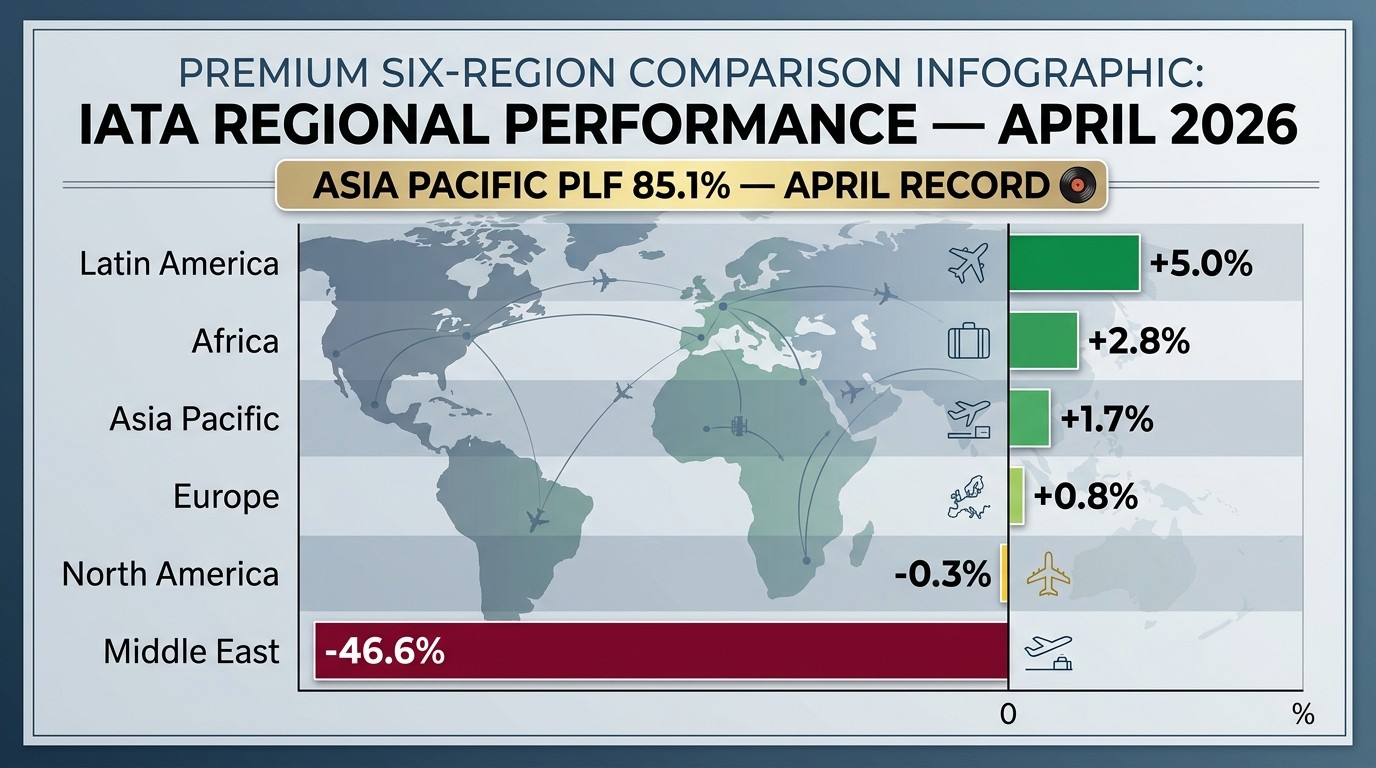

3. Regional Performance: Middle East -46.6% Collapse, Latin America +5.0% Leads

Region | RPK YoY | Notes |

|---|---|---|

Latin America & Caribbean | +5.0% | Strongest growth; international +8.9%, April-record PLF |

Africa | +2.8% | Continued reroute benefit from Middle East disruption |

Asia Pacific | +1.7% | Sharp deceleration from March's +11.3%; PLF 85.1%, April record |

Europe | +0.8% | Slowest positive growth |

North America | -0.3% | Pulled negative by domestic -0.6% |

Middle East | -46.6% | Eased from March's -59.2%; PLF 70.6% (-12.5 ppt) |

Middle East -46.6%: Worst is past, but normalization is far off

Middle East carriers improved from a -59.2% reading in March to -46.6% in April, with the partial US-Iran ceasefire contributing to the easing. The worst of the contraction has likely passed, but with May Middle East departure-and-arrival capacity forecast down -26.6%, short-term normalization isn't on the table. The variables that need to settle — airspace safety, hull insurance pricing, and the block-time penalty from rerouting — don't reset on a one-month timeline. Korean executives planning Saudi or UAE business travel between June and September should treat commercial scheduling as a risk variable rather than a given.

Asia Pacific: Growth decelerated, but PLF hit an April record

Asia Pacific cooled from +11.3% in March to +1.7% in April, but it remains the largest contributing region globally and posted an 85.1% load factor — the highest April reading on record. That means Korea-Japan, Korea-Southeast Asia, and Korea-China commercial routes ran near full through April, and that fullness is likely to persist into May. For principals departing Gimpo SGBAC or Incheon on short-haul international, premium cabin availability is already tight.

Europe +0.8%, North America -0.3%: Developed-market stall

Europe posted the slowest positive growth, and North America turned negative as the US domestic market softened. Some of this reflects Easter falling in early April, draining the late-month transatlantic peak. The question for May is whether the post-Easter normalization restores typical growth or whether reduced commercial supply persists. For Korean principals, the implication is the same either way: commercial schedule stability on Incheon-Americas and Incheon-Europe is materially worse than usual.

4. Route-Level Changes: Europe-Asia +15.3%, Middle East Routes Cut in Half

Strong international routes

Europe-Asia +15.3%: The strongest international route in April, sustaining the surge as direct traffic continues to absorb what used to transit Middle East hubs

Asia-North America +8.3%: The Korean transpacific corridor remains solidly in growth, which keeps it tight on commercial premium availability

Weak international routes

Middle East-Asia -40.5%: Korea-to-Middle East scheduled traffic has been cut roughly in half

Middle East-North America roughly -55%: US-to-Middle East commercial more than halved

North Atlantic -2.8%: Soft on the Easter timing shift into early April

Key domestic markets

Strongest: Japan +3.7%, Brazil +2.6%, China +1.2% (down from March's +13.7% as Lunar New Year effects faded)

Weakest: India -2.9%, US -0.6%, Australia -0.4% (sharp reversal from March's +8.8%)

5. May and June Forward Schedules: Recovery Pushed Out

Month | Seat Capacity YoY | Middle East Capacity YoY | Implication |

|---|---|---|---|

April (actual) | -0.8% | Sharply contracted | Recovery anticipated in March analysis did not materialize |

May (forecast) | -1.1% | -26.6% | Further deterioration from April |

June (forecast) | +0.2% | Volatile | Marginal recovery dependent on Middle East situation |

The May recovery that IATA's March analysis anticipated did not materialize. May seat capacity is now forecast down -1.1% YoY — worse than April's -0.8% — with Middle East departure-and-arrival capacity down a further -26.6%. June's expected +0.2% bump is too thin to constitute meaningful normalization and depends on the Middle East regional situation holding stable. For Korean principals, that means May commercial availability is contracting further from April, and the June recovery isn't enough to ensure summer pricing stability.

6. Five Charter Implications for Korean HNW Principals

Implication ① Incheon-Europe charter's structural advantage widens

Europe-Asia traffic is up +15.3% on the corridor, but the routing reality has changed. Commercial flights now reroute around closed Middle East airspace, adding 1-3 hours of block time. Ultra-long-range business aircraft like the G650ER and Global 7500 can fly Seoul-Europe non-stop via polar or Siberian routings, skipping the detour. Combined with tighter commercial premium availability in May, the time advantage on the Seoul-Europe corridor is materially larger for charter than it was a quarter ago. The dedicated Incheon long-haul reference is in the Incheon Long-Haul Guide.

Implication ② Lock in May's critical itineraries

With May capacity contracting further than April, the rational response is to lock in the principal's irreplaceable May flights — executive meetings, IPO roadshows, family travel — on charter. The right structure depends on volume: single charters for one-off trips, a 25 or 50-hour jet card for a month's worth of activity, or an annual program for principals carrying volume into June and beyond. For comparison across single charter, jet card, and annual program structures, see the Rental Cost by Duration Guide.

Implication ③ Shift Middle East travel to charter

With Middle East-Asia commercial down -40.5% and Middle East-North America roughly -55%, any Korean executive traveling to Saudi Arabia or UAE on commercial is operating with deteriorating service inventory. An Incheon-Dubai non-stop on a G650ER runs about 9 hours and approximately $180K-$380K per leg, and gives the principal complete control over departure timing and routing — important when May Middle East capacity is down -26.6%.

Implication ④ Gimpo short-haul charter for schedule control

Domestic markets are flat overall but with wide dispersion — Japan +3.7% on top, Australia reversing sharply on the bottom. For Korean executives running short-haul Japan, China, or Southeast Asia travel, where pricing and availability are likely to fluctuate, Gimpo SGBAC charter provides schedule control that commercial cannot match this quarter. For Gimpo charter detail, see the Gimpo SGBAC Guide.

Implication ⑤ Reaffirm the 6-12 month lock-in case

If H1 2026 is shaping up as an unusually unstable period for commercial schedule and pricing, the case for 6-12 month forward lock-in strengthens for any Korean principal flying five or more long-haul flights annually. Lock-in delivers four simultaneous benefits — 10-20% hourly rate concessions, priority aircraft and crew, seasonal-variance protection, and bundled BestTurn VIP escort. The full booking-process reference is in the 5-Step Booking Process Guide.

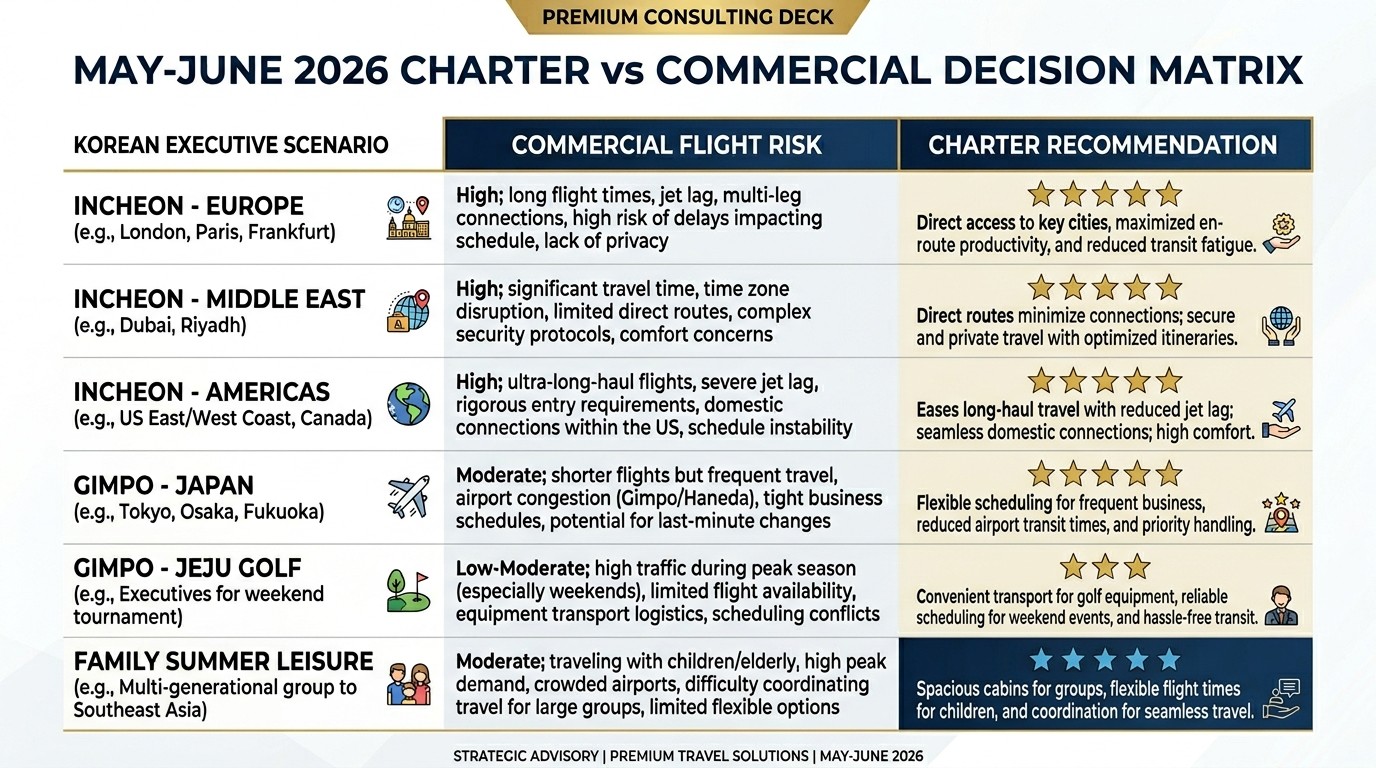

7. Commercial vs Private Charter: A May-June 2026 Decision Matrix

Travel Type | Commercial Risk | Charter Case |

|---|---|---|

Incheon-Europe executive travel | +1-3 hours block time on Middle East reroute, tight May premium availability | ⭐⭐⭐⭐⭐ Strong |

Incheon-Middle East business | Commercial down -40.5%, May capacity down a further -26.6% | ⭐⭐⭐⭐⭐ Strong |

Incheon-Americas IPO roadshow | Asia-North America +8.3% growth keeps premium availability tight | ⭐⭐⭐⭐ Strong |

Gimpo-Japan short-haul business | Asia Pacific PLF 85.1% means flights run full, schedule changes hard | ⭐⭐⭐⭐ Strong |

Gimpo-Jeju golf | Weekend domestic congestion, schedule flexibility limited | ⭐⭐⭐ Schedule-driven |

Family summer leisure (May-June) | Anemic June recovery, July-August peak pricing unstable | ⭐⭐⭐⭐ Lock-in case |

The matrix above is a general decision reference for May-June 2026, grounded in the April IATA data. The right call for any specific principal depends on itinerary detail, party size, and budget. ACK consultation runs the comparison against your actual itinerary and presents the best-fit option. For travel-purpose-driven charter selection, see the Purpose-Driven Charter Catalog.

8. The Korea-Departing Market in April and Its May Outlook

April environment for Korea-departing international

Asia Pacific decelerated to +1.7% in April but posted a record April PLF of 85.1%, which translates to a specific operational reality. Korea-Japan, Korea-Southeast Asia, and Korea-China commercial flights are running near full. First and business class availability ran tight through April and is likely to stay tight through May. For principals departing Gimpo SGBAC or Incheon on short-haul international, the premium cabin inventory available is meaningfully narrower than typical.

May priorities for Korean principals

Highest priority: Incheon-Europe executive travel and Incheon-Middle East business should shift to charter (commercial risk is highest)

Priority: Incheon-Americas IPO and multi-city itineraries warrant lock-in (Asia-North America +8.3% keeps premium tight)

Consider: Gimpo short-haul (Japan, China, Southeast Asia) charter for schedule control

Optional: Gimpo-Jeju golf and May-June family leisure on a 25-hour jet card

9. The ACK May-June Charter Advisory Process

Three-step engagement

Step 1 — Schedule intake: Share May-June travel or leisure dates, routing, party size, companions. NDA executed upfront

Step 2 — IATA data overlay: Itinerary commercial risk assessed against April IATA data; charter conversion priorities proposed

Step 3 — Quote and lock-in: Matched quotes from 3-5 global operators; single charter, jet card, or annual program options compared

Integrated BestTurn VIP escort

Once May-June charter dates are confirmed, BestTurn VIP Airport Escort integrates into the booking — Gimpo SGBAC departure (about 45-50 minutes), Incheon departure (about 100-130 minutes), or Jeju arrival (about 5-10 minutes). With commercial seat supply tight, combining the 5-minute Gimpo SGBAC processing or the 30-40 minute Incheon VIP customs lane with the charter itself compounds the time advantage further.

10. Frequently Asked Questions

Q: Will April's contraction extend into May?

IATA's May capacity forecast is -1.1%, worse than April's -0.8%, so the demand-and-supply contraction is on track to continue into May. June is forecast at +0.2%, a marginal positive that depends on the Middle East situation. Korean principals carrying May-June commercial-heavy itineraries are accumulating risk; building charter as a parallel option through this window is the prudent move.

Q: Is charter actually faster than commercial on Seoul-Europe right now?

Yes. G650ER and Global 7500-class aircraft can fly Seoul-Europe non-stop via polar or Siberian routings, picking the shortest viable path. Commercial widebodies are rerouting around closed Middle East airspace and adding 1-3 hours to block times. Charter delivers both a time advantage and full schedule control on this corridor — the broker builds the schedule around the principal, not the other way around.

Q: Is May-June Middle East business travel still feasible?

Middle East airspace remains volatile, but the trajectory from -59.2% in March to -46.6% in April suggests easing as the US-Iran ceasefire took partial effect. Charter operators assess airspace safety, insurance pricing, and rerouting individually, and ACK only matches ARG/US Gold or higher and Wyvern Wingman or higher-rated operators. Incheon-Dubai and Incheon-Doha are operating through June-September, but contract language allowing schedule flexibility is strongly recommended.

Q: How does April's data affect Korean carriers specifically?

Korean Air and Asiana sit within the Asia Pacific +1.7% region but are running at a record 85.1% load factor. The Incheon-Europe commercial routings are extended by Middle East airspace rerouting, and tighter premium cabin availability is pushing both pricing and inventory pressure on first and business class. Executive itineraries with high commercial dependence face real May-June schedule stress.

Q: Did charter pricing rise in April?

Higher fuel costs and longer reroutes are flowing through to some charter quotes. ACK quotes from matched global operators break out hourly rate and fuel surcharge separately, so pricing drivers are visible and traceable. Principals on a 6-12 month lock-in arrangement fix pricing at issuance and avoid the volatility; single charter clients should ask for variability ranges at quote stage as a matter of course.

Q: How do I start a May-June charter advisory?

Send routing, dates, and party size to ACK. Within 24-48 hours of NDA execution, you'll receive an itinerary commercial-risk analysis grounded in April IATA data, plus charter conversion priorities. First consultation is free, and quotes follow across single charter, jet card, and annual program options.

📞 Free May-June charter advisory

HNW and executive advisory: ACK — Request Quote | Wonjin Choi 📞 +82-10-7723-3177 | contact@aircharterkorea.com

VIP escort booking: BestTurn VIP Escort | Steve 📞 +82-10-3721-2853 | service@bestturnaround.com

🔗 ACK LinkedIn | Wonjin Choi LinkedIn

NDA upfront · IATA-data-driven commercial risk analysis · 3-5 global operator matched quotes · Integrated BestTurn VIP escort

Conclusion: What April's IATA Reading Means for Korean Principals

April 2026 is the recovery's first contraction. RPK -3.4%, international -5.3%, Middle East -46.6%: these aren't abstract aviation statistics, they're operational signals that hit Korean principals' May-June travel directly. Commercial seat supply is narrowing, Incheon-Europe flight times are extending, May capacity will contract further, and June recovery is thin enough that summer pricing won't normalize in time. An itinerary still resting on commercial first or business class through this window is exposed on three fronts simultaneously: schedule, availability, and pricing.

Charter resolves all three. The operator builds the schedule around the principal. Ultra-long-range aircraft pick the shortest viable routing, including Seoul-Europe non-stop without the Middle East detour. And pricing is fixed in the contract rather than left to market volatility. April's IATA reading isn't just industry data; it's a clear signal that, for Korean principals, locking in May's critical flights on charter is the operationally rational play.

ACK runs a single consulting channel that translates IATA monthly data into actual Korean principal flight decisions. From April-data-driven May-June planning through global operator matching through integrated BestTurn VIP escort, ACK operates every step. The principal provides itinerary; everything downstream runs through ACK. Send routing, dates, and party size and you'll receive an April-IATA-grounded commercial risk analysis with charter alternatives within 24-48 hours of NDA execution. First consultation is free, and in a quarter where commercial schedule stability is at its narrowest, that's the fastest path to preserving the principal's schedule freedom.

In the air: Air Charter Korea. On the ground: BestTurn. Together preserving principal schedule freedom across an unusually volatile first half of 2026. IATA publishes monthly; what makes that data actionable for a specific principal is the consulting that converts it into decisions. ACK is the independent broker running that translation in the Korean market.

✍️ About the Author

Wonjin Choi | Former Korean Air Business Jet Operations Manager · Former Samsung Electronics Business Jet Account Manager

Victor × Air Charter Service Korea Agent

Founder, Air Charter Korea

This guide draws on publicly released April 2026 Air Passenger Market Analysis data from IATA (the International Air Transport Association), official service information from Air Charter Korea, ARG/US and Wyvern global aviation safety frameworks, the Korean Aviation Safety Act and Aviation Business Act, and global business aviation market reference pricing as of May 2026. Market data is attributed to IATA's official releases, and May-June forward estimates reflect IATA's own forecasts. All pricing and market flows represent reference ranges; actual quotes, operator matching, and route availability vary with timing, operator policy, and airspace safety conditions. For exact quotes and advance booking, ACK consultation alongside operator official channels is the appropriate source. IATA, ARG/US, Wyvern, Victor, and Air Charter Service are registered trademarks of their respective organizations; this guide is provided for general informational purposes and does not reflect any affiliate relationship with the named bodies.