IATA March 2026 Air Passenger Market: Middle East -58.6%, Asia-Pacific PLF 87.2% All-Time High — Five Implications for Private Jet Charter

Key Takeaway

IATA's April 29 data release for March 2026 contains three signals that matter for anyone in private aviation.

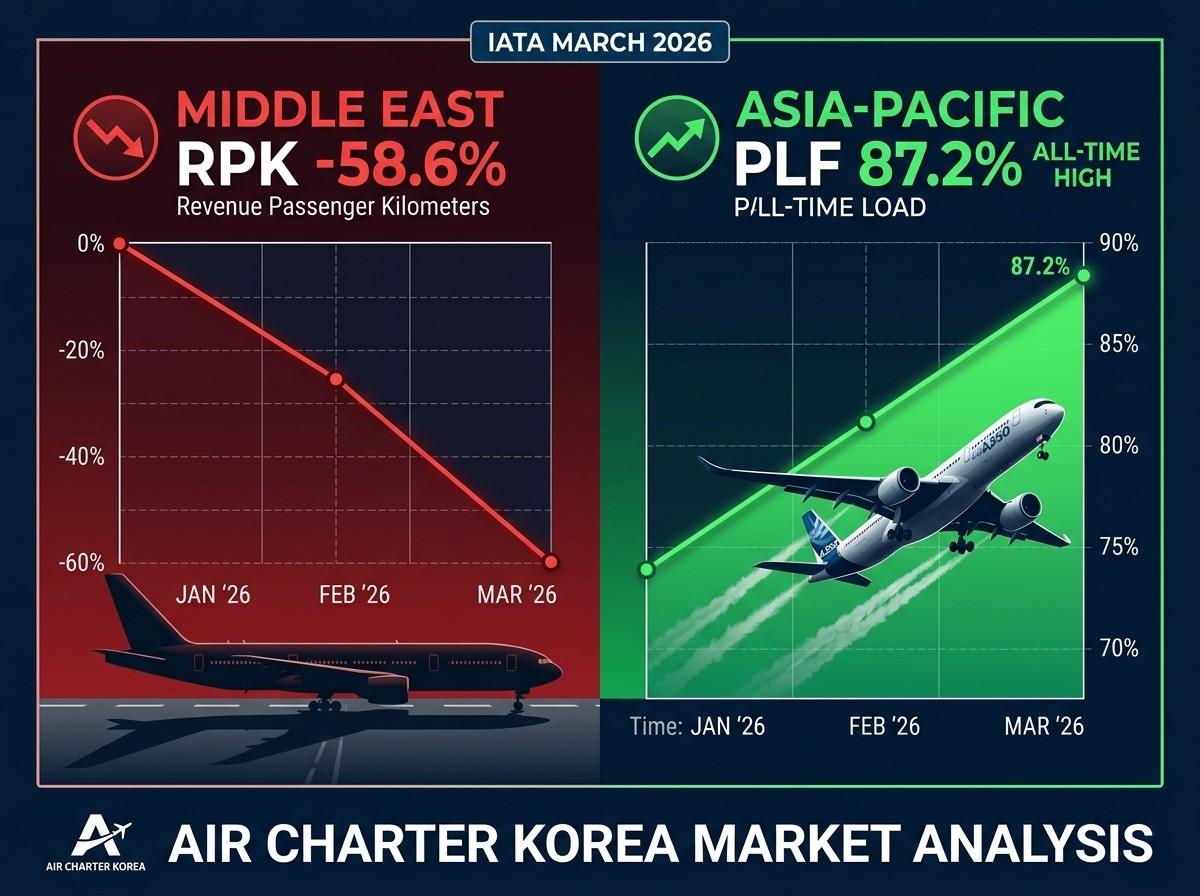

① Middle East RPK -58.6% — Iran conflict and airspace closures triggered the steepest regional decline since the pandemic. ASK -54.7%, PLF down to 68.3%.

② Asia-Pacific PLF 87.2% — All-time record load factor. RPK +11.5%, the largest regional contributor to global growth.

③ Europe-Asia +29.3% (PLF 93.6%) — Airlines added +14.9% capacity and flights were still almost full. Dubai and Doha connecting traffic is structurally migrating to Incheon, Singapore, and Hong Kong nonstops.

④ Jet fuel +106.6% YoY — 23-year high. Direct pricing pressure on charter operations.

This analysis breaks down what these numbers mean for private jet demand from Korea, charter pricing, and VIP airport escort at Incheon.

→ Request a Middle East bypass charter quote

IATA March 2026 Air Passenger Market: Middle East -58.6%, Asia-Pacific PLF 87.2% All-Time High — Five Implications for Private Jet Charter

On April 29, 2026, IATA released its March global air passenger data. The headline number — RPK +2.1% — is the weakest monthly growth since the pandemic. But the headline hides two completely different stories happening simultaneously. The Middle East aviation market is in structural collapse (-58.6%), while Asia-Pacific is posting the highest load factors in its history (PLF 87.2%). Strip out the Middle East and the rest of the world's international demand grew around +9%. The industry's underlying health is intact.

IATA Director General Willie Walsh framed it this way: "Demand for air travel continued to grow in March despite disruptions in the Middle East. The nearly 61% decline in international traffic by carriers in the Middle East did restrain global growth to 2.1%. Outside of the Middle East, demand grew by 8%."

This analysis, from the Air Charter Korea (ACK) consulting team, reads the IATA March data through the lens of private jet charter from South Korea and VIP airport escort at Incheon. Not a data dump — a practical breakdown of what these numbers mean for your business and your travel. The perspective comes from direct experience managing Korean Air BizJet operations, running Samsung Electronics' corporate aviation desk, and applying global market intelligence as the Victor × Air Charter Service Korea agent.

📞 Need a charter that bypasses Middle East airspace?

ACK provides optimized routing around restricted airspace, safety-verified operators, and all-in transparent pricing within 48 hours.

📧 contact@aircharterkorea.com | 📞 +82-10-7723-3177

→ Request a free quote

1. The Three Numbers That Run the Aviation Industry: RPK, ASK, PLF

Every IATA release, every airline earnings call, every aviation investor deck — three metrics appear on every page. Whether you're a graduate student studying the industry, a corporate travel manager, or a client considering a charter from Seoul, understanding these three terms unlocks the entire data set.

RPK (Revenue Passenger Kilometers) — Demand

"How many kilometers did paying passengers actually fly?" Calculated as revenue passengers multiplied by distance flown. Two hundred passengers on a Seoul–Jeju flight and two hundred on an Incheon–LA flight register the same headcount but wildly different RPK — which is why RPK captures real market value better than passenger numbers alone.

ASK (Available Seat Kilometers) — Supply

"How many kilometers did available seats fly?" An A330 with 290 seats operating Incheon–Bangkok (3,720 km) generates 1,078,800 ASK — whether those seats sold out or flew empty.

PLF (Passenger Load Factor) — Efficiency

"What percentage of available seats were actually sold?" RPK ÷ ASK × 100. Above 80% = healthy. Above 85% = tight. Above 90% = effectively full. The key relationship: when RPK grows faster than ASK, PLF rises — and airline profitability improves.

Segment | RPK (YoY) | ASK (YoY) | PLF | Reading |

|---|---|---|---|---|

Total | +2.1% | -1.7% | 83.6% | Demand up, supply down → all-time March PLF record |

International | -0.6% | -6.2% | 84.1% | First decline since March 2021 — Middle East distortion |

Domestic | +6.5% | +5.6% | 83.0% | China and Brazil double-digit, driving the segment |

The standout detail: international RPK went negative for the first time since March 2021. But this minus is entirely a Middle East artifact — strip out that region and international traffic grew approximately +9%, with PLF rising in every other region.

2. Regional Scorecard: The Middle East Crater and the Asia Surge

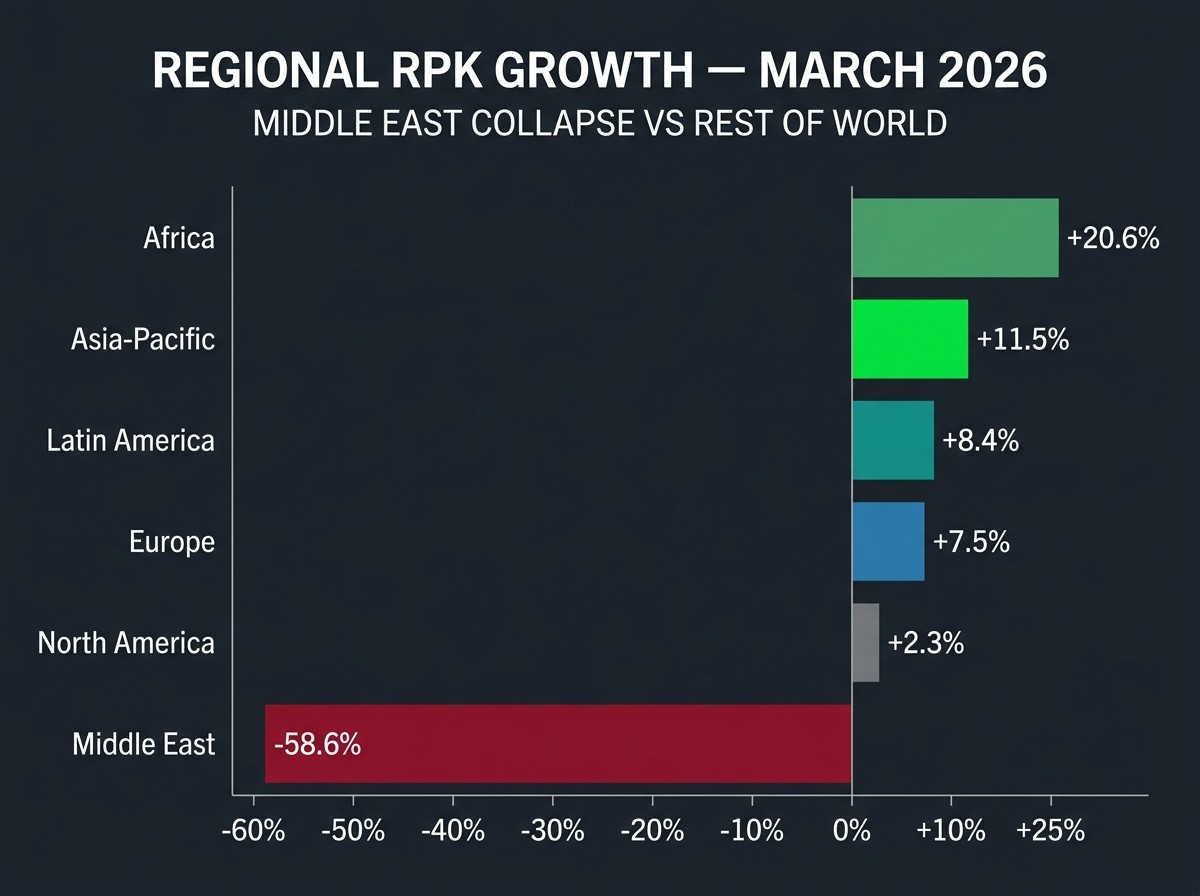

Region | RPK (YoY) | PLF | Key Reading |

|---|---|---|---|

Africa | +20.6% | 76.2% | Eight straight months above global average. Low PLF = room to grow. |

Asia-Pacific | +11.5% | 87.2% ★ | Largest contributor to global growth. All-time record PLF. |

Latin America | +8.4% | — | Brazil +10.8%, four consecutive double-digit months. |

Europe | +7.5% | — | Europe-Asia +29.3% (PLF 93.6%) — nearly full despite +14.9% capacity add. |

North America | +2.3% | 83.7% | Steady. U.S. domestic +1.4%. |

Middle East ⚠️ | -58.6% | 68.3% | Airspace closures. ASK -54.7%. PLF -6.3 ppt. Demand falling faster than supply. |

📊 Reading the data at a glance:

• Middle East: RPK -58.6%, ASK -54.7%, PLF 68.3% → demand falling faster than supply, efficiency deteriorating

• Asia-Pacific: RPK +11.5%, ASK +6.0%, PLF 87.2% → demand outpacing supply, load factors accelerating toward full

• Europe-Asia: ASK +14.9%, PLF 93.6% → airlines added almost 15% more seats and flights were still nearly full

3. Middle East Airspace Closures: What's Happening and Why It Matters

The Iran conflict and associated airspace restrictions are the single largest disruptor in the 2026 global aviation market. The Gulf superconnector model — Emirates (Dubai), Qatar Airways (Doha), Etihad (Abu Dhabi) as waypoints on the Kangaroo Route between Europe, Asia, and Australia — is under severe strain. Traffic that used to flow through those hubs is being rerouted.

Scale of the impact

Metric | Figure |

|---|---|

Middle East airline international RPK | -60.8% |

Middle East total ASK | -54.7% |

Middle East PLF | 68.3% (↓6.3 ppt) |

April global seat forecast | -0.7% (Middle East -38.4%) |

May recovery forecast | +2.0% (Middle East still -18.3%) |

Jet fuel (YoY) | +106.6% ⚠️ — 23-year high |

Walsh's message to regulators was pointed: stabilizing jet fuel supply and pricing is essential, and airlines need slot flexibility given the extraordinary airspace capacity constraints. The fact that the IATA Director General is publicly raising fuel rationing as a realistic scenario tells you how serious this is.

Routes absorbing the displaced traffic

Route | RPK (YoY) | PLF | Reading |

|---|---|---|---|

Europe–Asia | +29.3% | 93.6% | +14.9% capacity added, still nearly full. Structural shift. |

North America–Asia | +12.2% | — | Pacific route demand recovering. |

Australia–Asia | +21.1% | — | Kangaroo Route bypass demand concentrating in Asia-Pacific. |

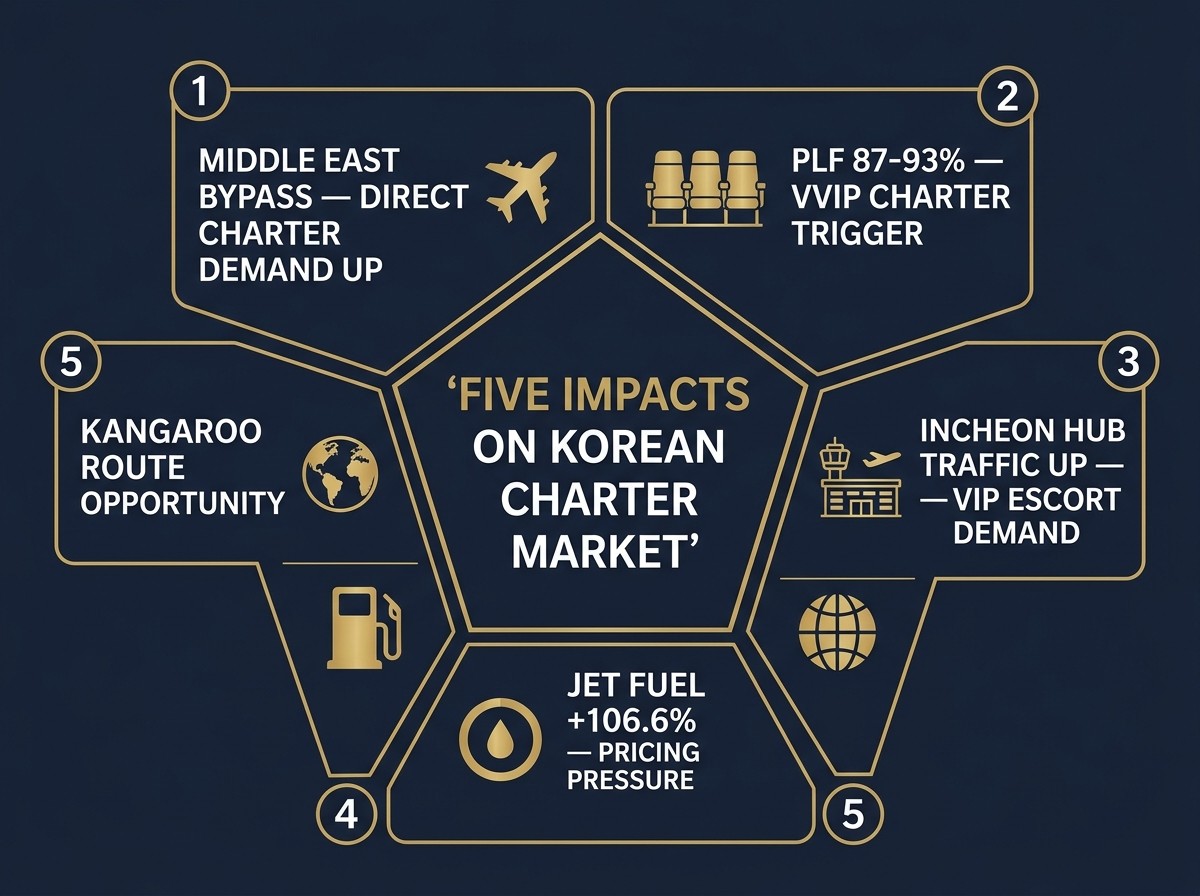

4. Five Ways This Data Affects the Private Jet Charter Market

Here's where the ACK lens comes in. Five specific impacts we're reading from the March numbers.

Impact ① Middle East airspace risk → direct charter demand from Korea to Europe/Africa rising

Korean corporate VIPs and ultra-high-net-worth clients are already moving away from Dubai and Doha connecting itineraries. A Seoul–London nonstop on a G650ER (roughly 12 hours, $138K–$450K) is faster and safer than a 15–18 hour commercial business-class connection through a Gulf hub — and it avoids restricted airspace entirely. We've seen this conversion pattern before: 2014 Ukraine crisis, early 2020 pandemic. The longer the Middle East airspace risk persists, the more structural the shift becomes. Full route details in our Seoul Route Guide.

Impact ② PLF 87–93% → commercial seats scarce → VVIP charter conversion

Asia-Pacific PLF 87.2%. Europe-Asia PLF 93.6%. Those numbers mean commercial first and business class are essentially sold out on the routes that matter — and it gets worse in the European summer season (May through August). PLF above 90% is a structural trigger for corporate executives, entertainers, and government officials to move from commercial aviation to charter. For cost comparison between commercial and charter, see our Membership vs. Charter Cost Analysis.

Impact ③ Incheon transit traffic surging → VIP escort demand expanding

As Dubai and Doha connecting traffic migrates to Incheon, international transit volumes are structurally increasing — particularly Europe↔Southeast Asia/South Asia bypass flows. When every arriving widebody is at 90%+ load factor, immigration queues get longer and terminal congestion rises. The value of BestTurn VIP Airport Escort's physically separated routing through Incheon becomes more acute in exactly this environment. VIP escort inquiries: Steve (📞 010-3721-2853). Full details in our Incheon VIP Escort Guide.

Impact ④ Jet fuel +106.6% → charter pricing pressure

Jet fuel up 106.6% year-on-year to a 23-year high. Asia and Europe — the regions most dependent on Gulf refinery supply — face potential fuel shortages in the months ahead. This puts direct upward pressure on charter pricing. ACK addresses this through our transparent pricing model: fuel is itemized as a separate line, based on projected departure-day costs, with no post-flight fuel surcharge adjustment. The quoted total is the settlement total.

Cost mitigation strategies remain effective regardless of the fuel environment: round-trip booking (20–40% savings), empty legs (50–90%), multi-operator competitive quotes, right-sized aircraft selection. Route pricing reference: Price Comparison Guide.

Impact ⑤ Asia-Pacific Kangaroo Route charter opportunity expanding

Australia–Asia RPK +21.1% signals that Kangaroo Route bypass demand is concentrating in Asia-Pacific. Incheon has the potential to emerge as a waypoint hub on this rerouted flow. ACK is leveraging our Southeast Asian partner network (Luxaviation, ExecuJet, Sapura Aero) to position for Asia-Pacific Kangaroo Route charter brokerage. For our global network structure, see the Provider Comparison Guide.

✈️ Did You Know? When Middle East airspace risk extends beyond a quarter, the "commercial avoidance → charter conversion" pattern reliably follows for VVIP and corporate clients. We observed this during the 2014 Ukraine crisis and the early months of the 2020 pandemic. ACK is already seeing month-over-month increases in Korea-origin direct charter inquiries to Europe and Africa.

5. Domestic Market Trends: China +13.7%, Japan +4.8%, India the Only Minus

Country | Domestic RPK (YoY) | Key Driver |

|---|---|---|

China | +13.7% | Lunar New Year + Lantern Festival effect |

Brazil | +10.8% | Four consecutive double-digit months |

Australia | +8.8% | Rebound momentum |

Japan | +4.8% | Steady growth — positive signal for Korea-Japan charter demand |

USA | +1.4% | Stable |

India | -1.0% | Only negative — Gulf worker flight disruptions impacting domestic feeder demand |

From a charter perspective, China at +13.7% and Japan at +4.8% confirm that Korea-China-Japan cross-border charter demand remains healthy. Gimpo–Tokyo Haneda, Gimpo–Osaka, Gimpo–Shanghai are ACK's core market — airport-specific details are in our Airport-by-Airport Charter Guide.

During the Korean Air BizJet years, Gimpo–Haneda was our single highest-frequency route. Japan's +4.8% growth tells me their business aviation market is also in expansion mode, which means Haneda TIAT and Narita FBO slot availability will be a variable to watch. And from my Samsung Electronics corporate aviation days, I learned firsthand that when Chinese domestic traffic surges into double digits, business jet availability inside China tightens — meaning positioning costs for Korea-origin China-bound charters tend to creep up.

📊 Did You Know? South Korea has roughly a dozen registered business jets. The U.S. has around 22,000, China about 200, Japan approximately 80. Most Korea-origin charters therefore rely on positioning aircraft from other countries — and when those countries' domestic demand surges, the available pool tightens. China's +13.7% has direct implications for Korean charter positioning costs.

6. Bonus: Air Cargo Is Also Feeling the Middle East Shock

The cargo data released the same day shows the Middle East impact rippling through freight markets. Global cargo demand (CTK) contracted under the weight of airspace closures, while jet fuel at +106.6% drove cargo yields up +18.9%. Middle East and African carrier cargo capacity dropped sharply, and Asia-Europe freight routing is being restructured in real time.

Korea's semiconductor, display, and biotech industries are heavily dependent on air freight, and disruption to the Dubai DWC–Europe cargo corridor affects AOG (Aircraft on Ground) emergency parts shipments. ACK handles not only passenger charter but also heavy-lift cargo charter for Korean industry, including Middle East bypass freight routing.

7. May Outlook: Recovery or Structural Realignment?

IATA projects a slight global seat contraction of -0.7% in April (Middle East -38.4%), followed by a +2.0% recovery in May. The Middle East remains constrained at -18.3% even in May. Walsh's central message: "The summer is shaping up to be a normally busy time for travel. That's positive news, but airline resilience is being tested and stabilizing the supply and price of fuel is crucial."

The core question: is this a temporary disruption or a structural shift? Based on what I observed as the Victor × Air Charter Service Korea agent, the rerouting of Europe-Asia traffic away from Gulf hubs is already structural. Airlines don't add +14.9% capacity on direct Europe-Asia routes as a short-term patch — that's a medium-term fleet deployment decision. Even if Middle East airspace reopens fully, a meaningful share of the traffic that has shifted to nonstop routings won't come back.

Incheon's emergence as a bypass hub is a medium-term trend, not a short-term blip. That's structurally positive for both ACK's Incheon-origin long-haul charter business and BestTurn VIP Escort demand.

On the long view: IATA's Long-Term Demand Projections (released March 17, 2026) forecast global passenger RPK more than doubling from 9 trillion in 2024 to 20.8 trillion by 2050, a 3.1% compound annual growth rate. The historical moderation — 6.1% CAGR in 1972–1998, 4.5% in 1998–2024, 3.1% projected for 2024–2050 — reflects market maturity, not demand decline. Asia-Pacific is the largest growth engine. The long-term trajectory for private aviation in Korea is firmly upward.

🌍 Did You Know? IATA's Long-Term Demand Projections model global RPK reaching 20.8 trillion by 2050 — more than double the 9 trillion recorded in 2024. Asia-Pacific is projected to be the single largest driver of that growth, and Korea's private aviation market is riding that trajectory.

8. How ACK Is Responding to This Market Environment

① Expanding Europe and Africa direct charter capacity

We're broadening our operator pool for Seoul–London, Seoul–Paris, and Seoul–Frankfurt nonstop charters that bypass Middle East airspace. Only operators verified against ARG/US, Wyvern, and IS-BAO standards are included. Safety verification details: Safety, Insurance & Contract Guide.

② Scaling VIP escort at Incheon

BestTurn VIP Escort is expanding service capacity in response to rising Incheon transit traffic. As full flights become the norm and terminal congestion increases, the value of a physically separated routing grows exponentially. Escort inquiries: Steve (📞 010-3721-2853).

③ Reinforcing transparent quoting in a high-fuel environment

With fuel up 106.6%, the fuel line on a charter quote is now a material variable. ACK's Quote Transparency Guide explains how we itemize fuel separately, based on projected departure-day costs. No post-flight fuel adjustment. The quoted total is the settlement total.

9. Frequently Asked Questions

Q: What are RPK, ASK, and PLF?

RPK = demand (passengers × distance). ASK = supply (seats × distance). PLF = efficiency (RPK ÷ ASK × 100). 80%+ healthy, 85%+ tight, 90%+ full.

Q: Why was March's global growth only +2.1%?

Middle East -58.6% dragged the global number down. Excluding the Middle East, international traffic grew ~9%. The underlying market is strong.

Q: Why does PLF 87–93% boost charter demand?

Full flights mean commercial first and business class are scarce — particularly in peak season. That's a structural trigger for VVIP clients to convert to charter.

Q: How do Middle East airspace closures affect Korean charter?

Clients avoiding Gulf hub connections are requesting nonstop charters from Korea to Europe and Africa. ACK provides optimized bypass routing and safety-verified operator matching.

Q: How do I book a charter?

Contact ACK with route, dates, headcount. Safety-verified all-in quotes in 48 hours. No membership, single trips welcome.

Q: What does a charter from Seoul cost?

Jeju: $6K–$15K. Tokyo: $15K–$42K. Singapore: $60K–$115K. London: $138K–$450K. Full breakdown: Price Comparison Guide.

📞 Need a Charter That Avoids Middle East Airspace?

ACK provides optimized bypass routing + safety-verified operators + all-in transparent pricing within 48 hours.

📧 contact@aircharterkorea.com | (Wonjin 📞 +82-10-7723-3177)

🌐 ACK — Request a Quote | BestTurn VIP Escort (Steve 📞 010-3721-2853)

🔗 ACK LinkedIn | Wonjin Choi LinkedIn

24/7 · 365 days · Free consultation · No membership · ARG/US · Wyvern · IS-BAO pre-verified

Conclusion: What the Data Says — and What to Do About It

The March IATA data tells two stories at once. One is risk: Middle East -58.6%, jet fuel +106.6%. The other is opportunity: Asia-Pacific PLF 87.2% all-time high, Europe-Asia +29.3%, Incheon emerging as a bypass hub. In private aviation, risk and opportunity are the same coin — just different sides. When commercial flights are full, when legacy connecting routes carry geopolitical risk, when fuel prices spike — that's precisely the environment where a private jet delivers the most value.

Air Charter Korea monitors this market in real time and provides clients with the safest, most cost-effective charter options — quoted transparently. BestTurn completes the ground experience at Incheon.

The data is talking. Time to move.

✍️ About the Author

Wonjin Choi | Founder, Air Charter Korea

Former Korean Air Business Jet Operations Manager · Former Samsung Electronics Business Jet Account Manager

This analysis is based on IATA's "Air Passenger Market Analysis — March 2026" and "Air Cargo Market Analysis — March 2026" data released April 29, 2026, with market interpretation by Air Charter Korea. All statistics are per IATA official release. Charter pricing represents market reference ranges. IATA source: IATA Press Release (April 29, 2026)

Published: April 30, 2026 | Data source: IATA Air Passenger Market Analysis, March 2026 (released April 29, 2026) | Read time: 15 minutes